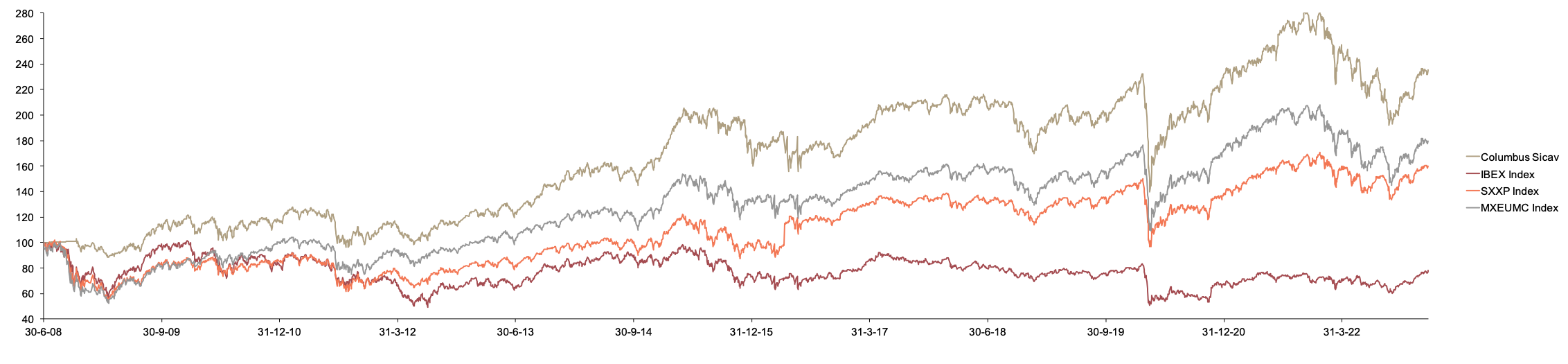

Pareturn GVC Gaesco Columbus European Equity Fund class I2 is down 0.36% in August 2024, while up 5.8% over the past six months. August has been a volatile month in the markets, but Columbus has performed steadily. Since its inception in June 2008, the Columbus I2 class has gained 148%, outperforming European equity indices.

August was a difficult month for the markets for various reasons, such as the situation in Japan and employment in the US. The stock markets suffered a sharp correction in the first days of the month (Stoxx50: -6%, Nasdaq: -8%), although they recovered as the days went by. This correction is an indication that the valuations of some assets, especially in the US technology sector, are excessive. At the same time, the US economy is showing signs of exhaustion.

Fortunately, the interest rate cycle is about to turn, which provides good support for the markets and smallcaps in particular. In Europe, valuations are more than reasonable, and we continue to find a lot of value in good European companies that manage to grow globally in a not entirely favorable macroeconomic environment, with very good returns on capital and solid cash flow generation. In August, we have had a good performance in relevant positions such as Kinepolis (+9%), Reply (+9%), YouGov (+8%) and Dalata (+7%). We have also seen a significant rebound in two positions that until now had penalized us: Mobico (+21%), which released good results, and Grifols (GRFB +16%, GRFA +8%), where the process for a potential takeover bid continues. On the negative side, this month has been difficult for Teleperformance (-17%) due to a change of management, and Trainline (-11%) and Kontron (-14%) also fell despite reporting good results.

In August, we have had a good performance in relevant positions such as Kinepolis (+9%), Reply (+9%), YouGov (+8%) and Dalata (+7%). We have also seen a significant rebound in two positions that until now had penalized us: Mobico (+21%), which released good results, and Grifols (GRFB +16%, GRFA +8%), where the process for a potential takeover bid continues. On the negative side, this month has been difficult for Teleperformance (-17%) due to a change of management, and Trainline (-11%) and Kontron (-14%) also fell despite reporting good results.

We have initiated new positions in the portfolio which we will discuss in the coming months. We are also reducing our exposure to the financial sector.

Download monthly factsheet [PDF]

Since May 2023, Spanish investors can access the Columbus strategy through the Spanish fund GVC Columbus European Equities FI. The Fund can be purchased through the AllFunds, Inversis and Fundsettle platforms. Columbus has a Master-Feeder structure. The Pareturn GVC Gaesco Columbus European Equity Fund in Luxembourg (master) and the GVC Columbus European Equities FI (feeder). The Luxembourg vehicle offers institutional and retail share classes denominated in euros and sterling.