Annual letter to co-investors in GVC Columbus:

The year 2025 has been positive for our fund GVC Columbus and for global stock markets, although for many investors the depreciation of the US dollar (-12.5%) has eroded a good part of returns. The S&P 500 was up 16.4% (barely up 4% in euros), the Nasdaq 20.5% (7% in euros), while the Stoxx 600 in Europe was up 19.6%.

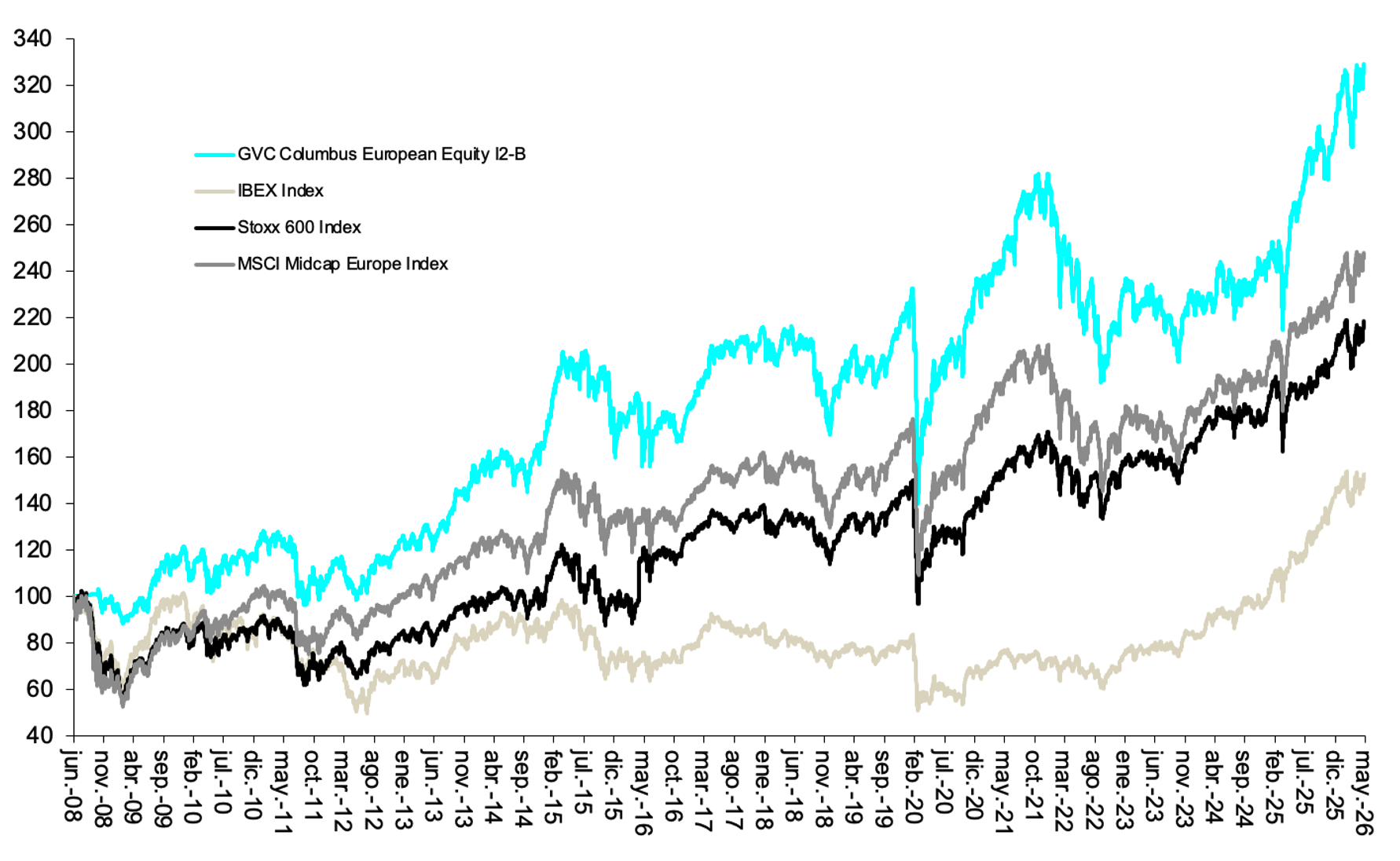

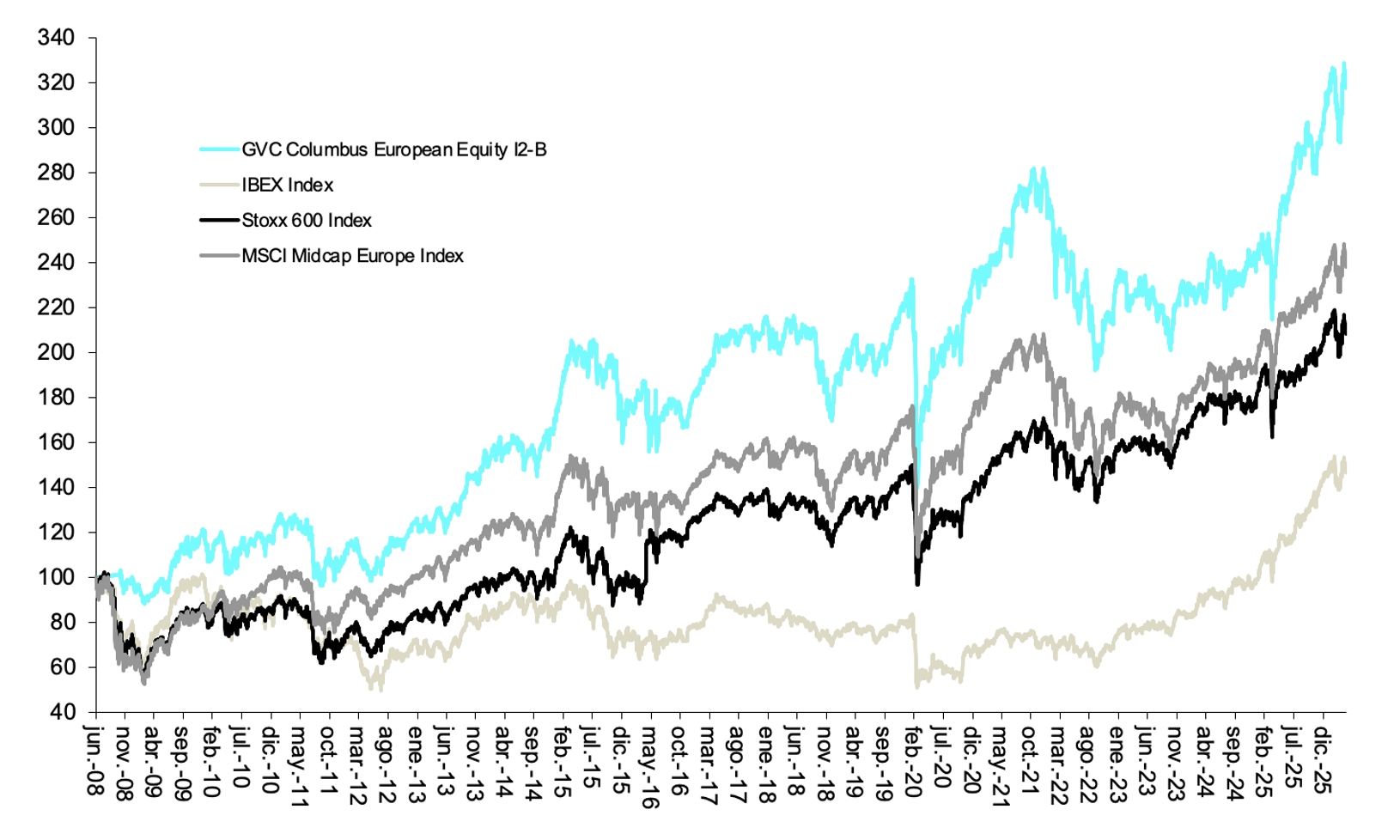

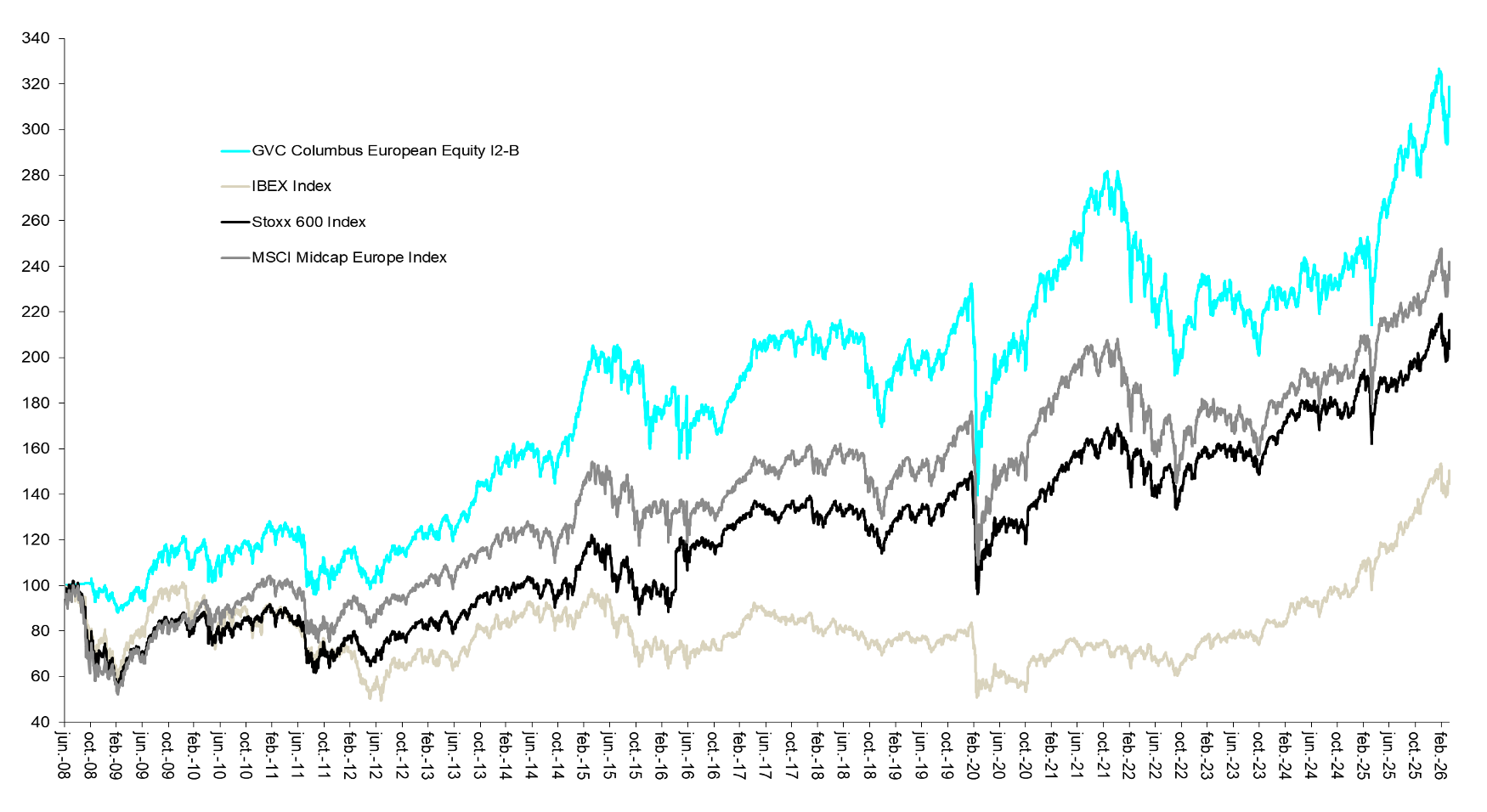

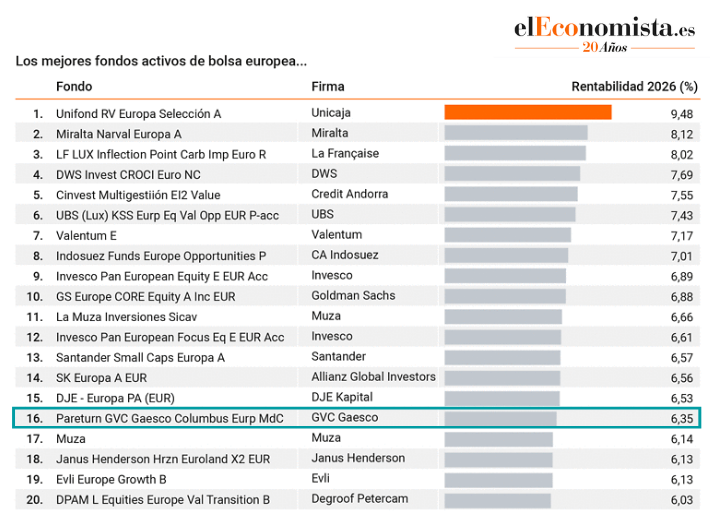

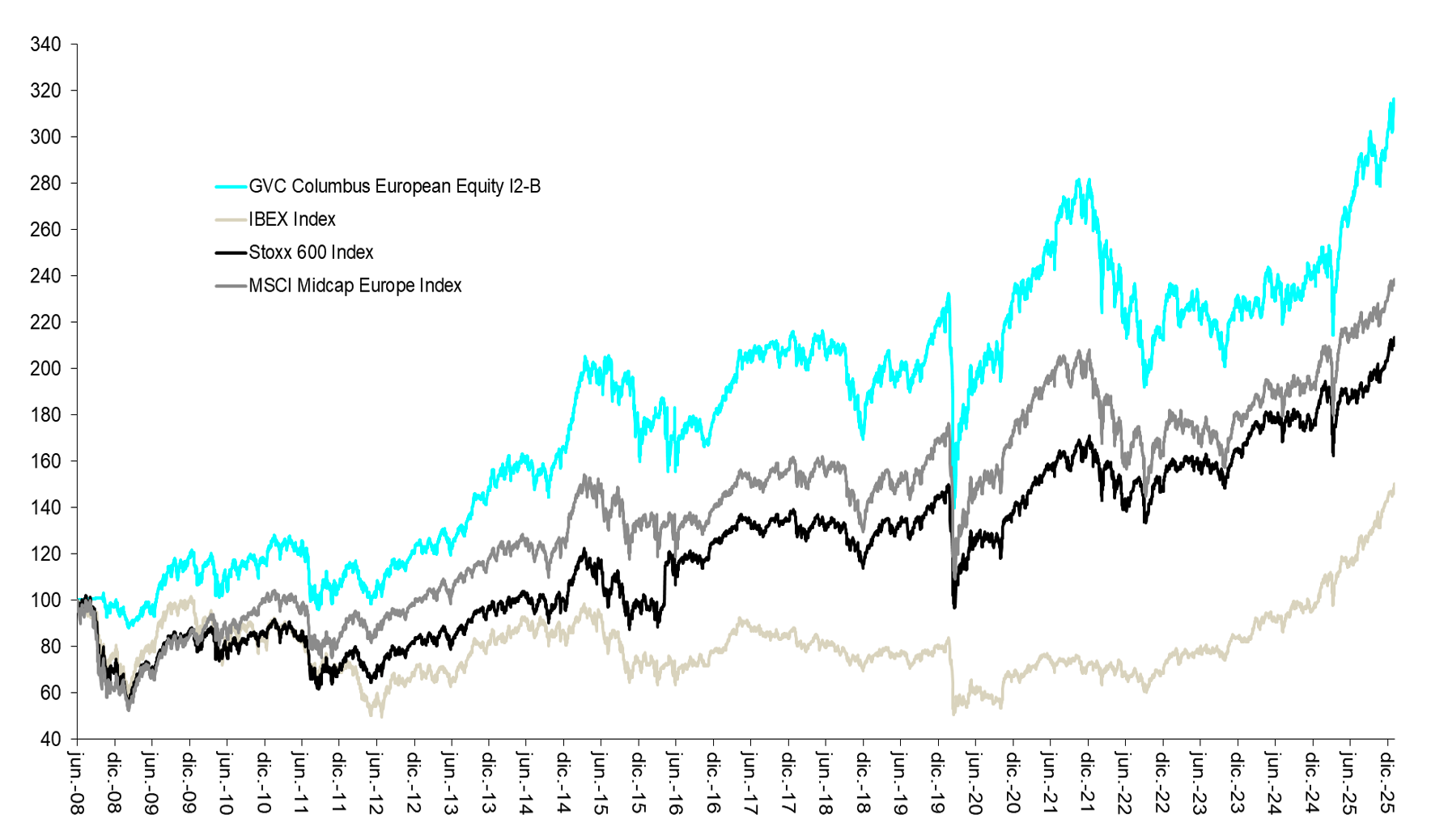

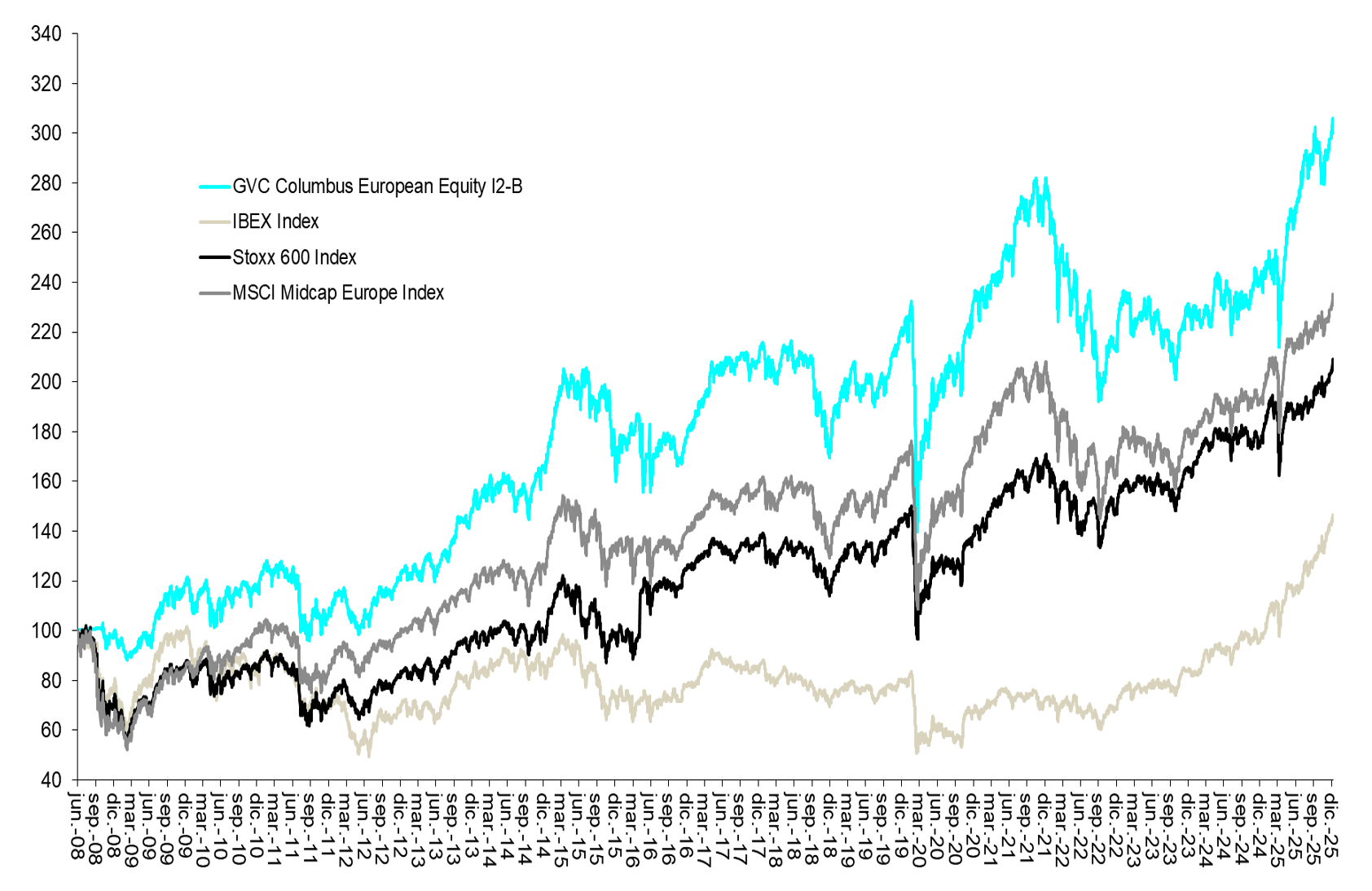

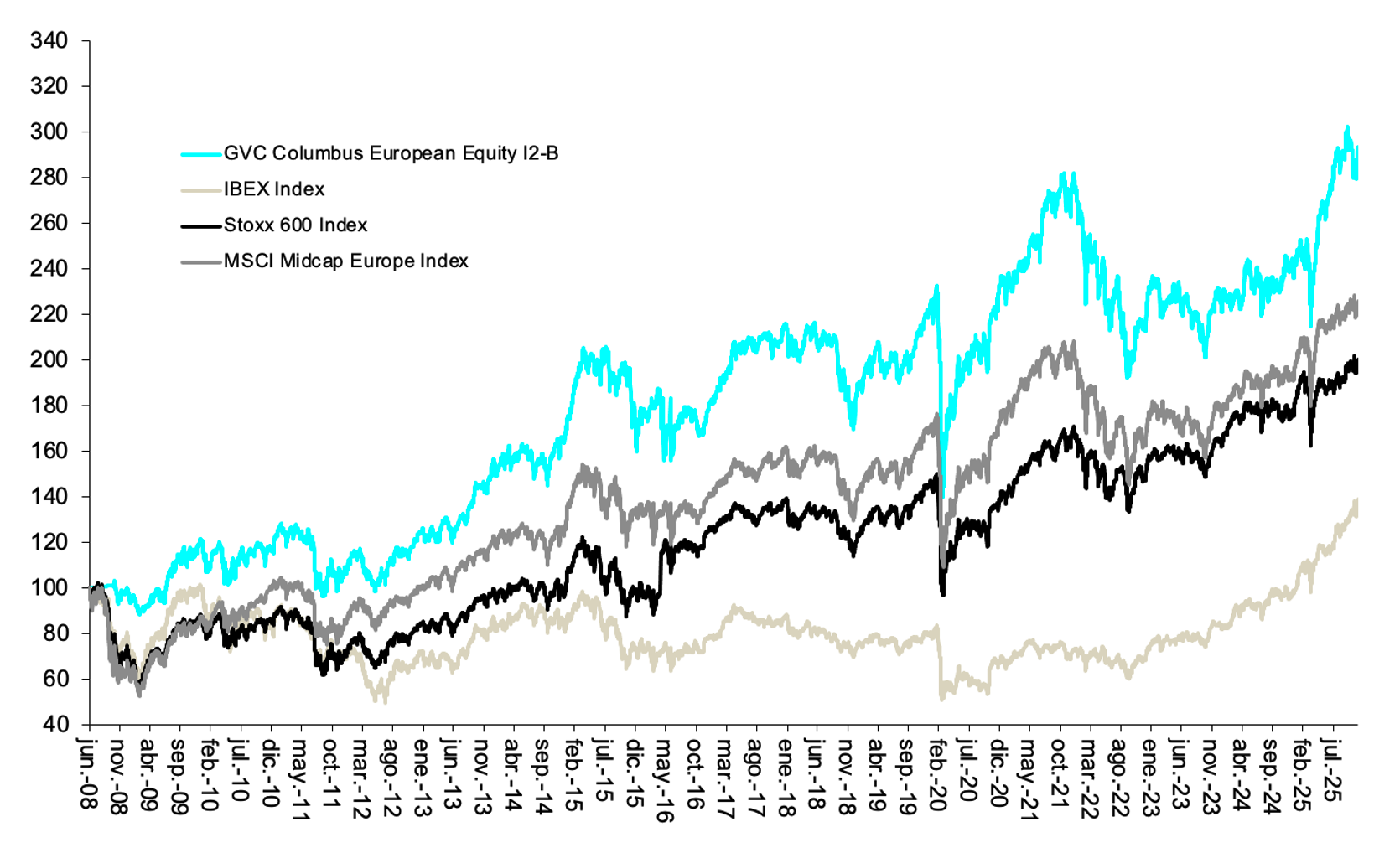

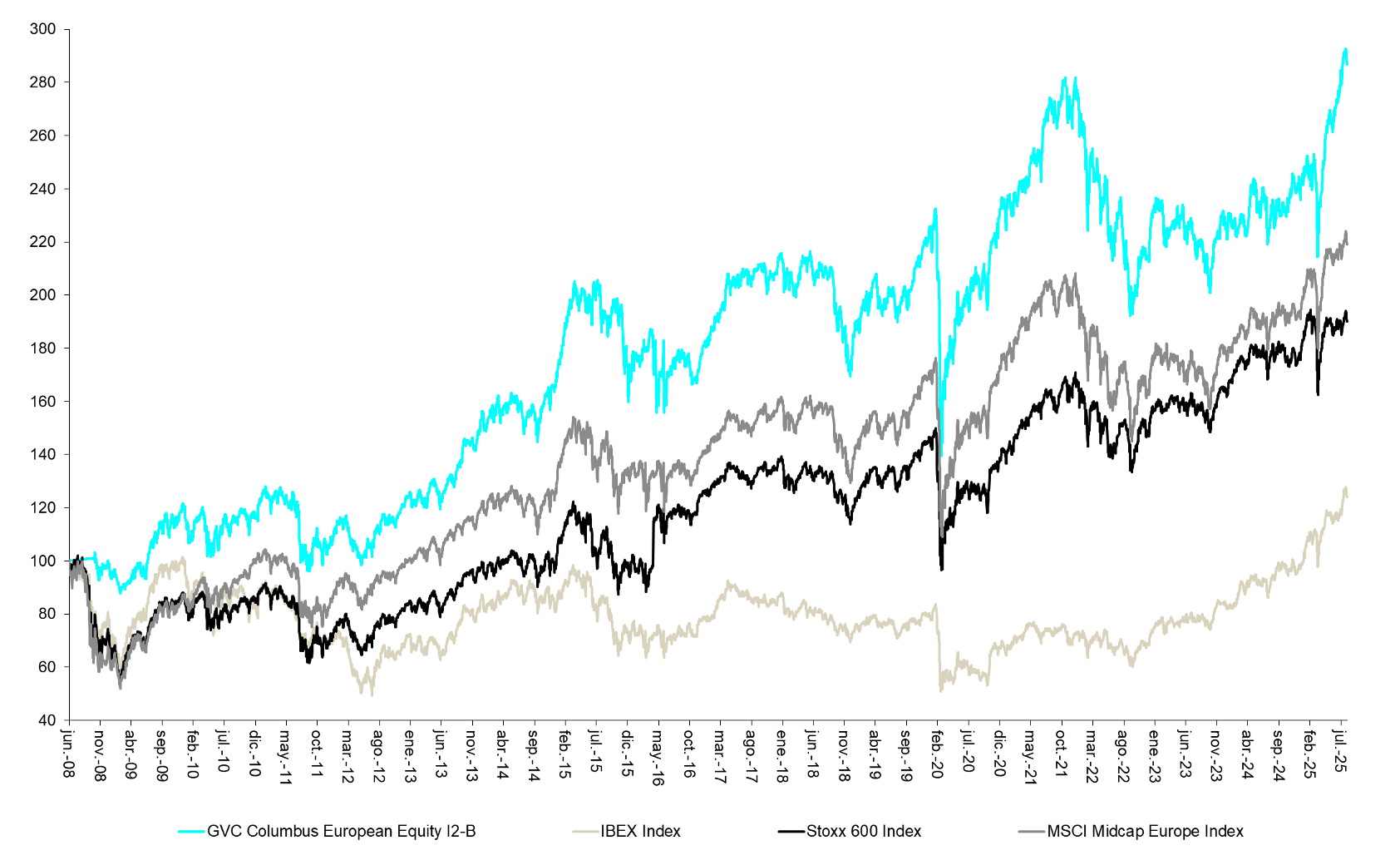

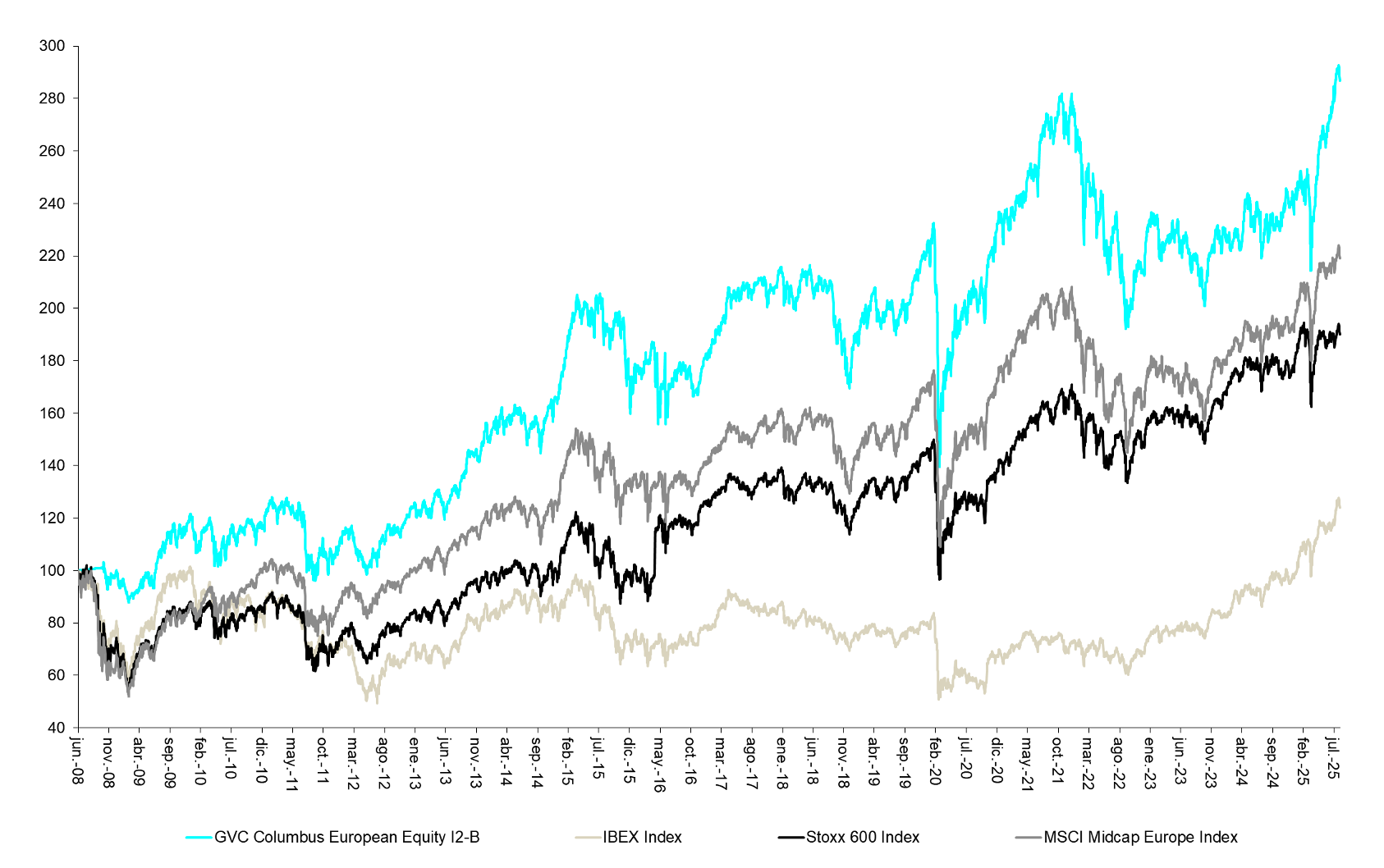

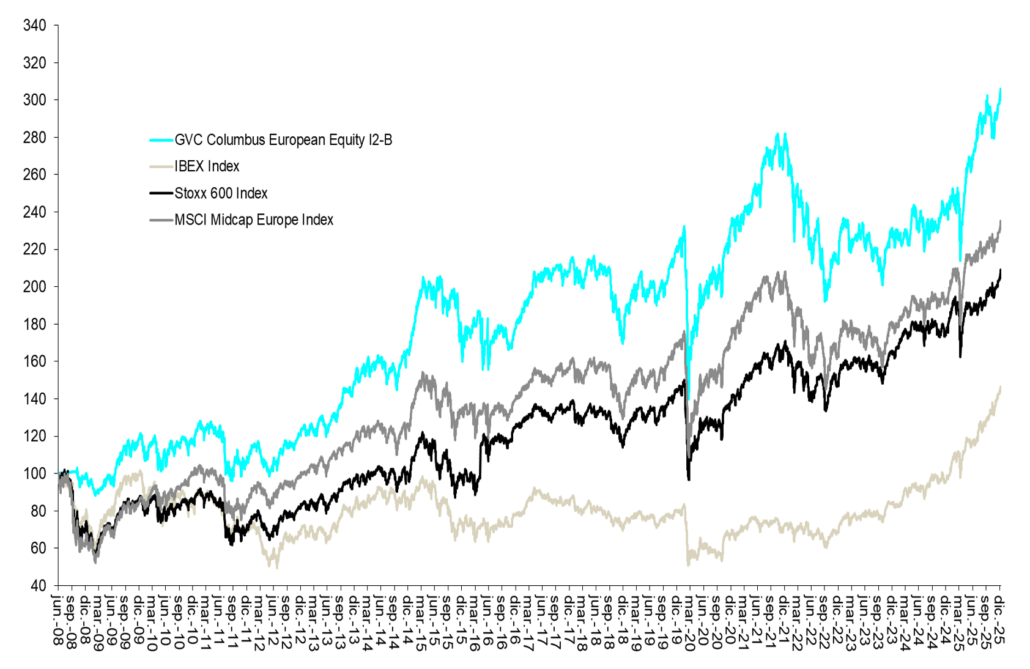

At Columbus we have had a good year. GVC Columbus European Equity fund class I is up 25.2% in 2025, above the Stoxx 600 which, as mentioned, is up 19.6% for the year. If we compare it with funds in our category (European mid caps), both Morningstar and Citywire show that the fund is in the top decile for the year and in the upper range of the first quartile over 3 and 5 years.

The fund’s objective is to buy medium-capitalization stocks in European markets with high revaluation potential, mostly quality companies with competitive advantages. We invest in companies with a good management team aligned with shareholders, as well as healthy balance sheets and cash generation. We complement the fund with some opportunities in stocks that, while not meeting all our quality criteria, have some catalyst for improvement and high upside.

Why mid caps in Europe? In European markets there are many very high-quality companies; they are not purely European businesses, as they compete all over the world. And they have an important advantage: they operate under very high legal and corporate governance standards. This is the market we know best after more than 30 years working in European markets; in many cases we know well their management teams, their track records, and core shareholders.

A very active year: this year we have met with more than 100 listed companies, in many cases several times with the management teams of our holdings to follow them closely. Close follow-up with management is, in our view, vital when investing. We currently hold around 35 companies in the portfolio, and we have a solid pipeline of potential ideas that could become good investments.

A concentrated fund: Investing in mid caps naturally has a growth bias; ideally, these are companies with the potential to become large businesses in the long term. Columbus has a blend style, its not exactly a “growth” fund: there are some value ideas with catalysts in the portfolio, and for growth stocks we pay close attention to valuations. At times we take advantage of market inefficiencies and we believe it is very important to avoid value traps, because technology is accelerating disruption and the development of new business models.

On the market environment: AI bubble? end of US exceptionalism? etc. This year two topics have dominated market sentiment: 1) The debate about the end of American “exceptionalism” is very relevant. There is growing doubt as to whether the US can continue financing a high public deficit (around 7% of GDP) at low cost. The market has already taken a stance to some extent: the US dollar has devalued, and long-term US yields are rising. The market is demanding higher yields from the US than from Europe, where rates are being cut and it is cheaper for governments and companies to finance themselves. Even if European reforms are taking too long, the US cycle is showing signs of exhaustion and it will be difficult to stimulate it further without damaging funding costs. Inflation has had a devastating impact on disposable income and real assets. Moreover, the valuation gap between the US and other markets remains excessive: the S&P 500 trades at 30x earnings versus 15x for the Stoxx 600, or 14x for the MSCI Mid Cap Europe. 2) On AI. On this topic it is very hard to know whether generative AI will reach significant levels of autonomy and which companies will monetize the opportunity. However, we do know that the capex for the 7 large US tech companies (c3.5tr in the 2025–30 period) is unlikely to generate an acceptable return on capital. Several reports have already sounded the alarm on this issue. Risk/reward profile for the US market is less appealing, while selected European names are attracting global flows.

On the cost of capital… the world has changed: after the inflationary spiral of the 1970s up to 2021, rates remained at extremely low levels and central banks have expanded their balance sheets to the extreme. During this period inflation remained relatively contained until the post-COVID hangover arrived. Today inflation appears to be under control (3% in the US, 2% in the EU) but not fully. Many data points suggest that monetary expansion and the rate cycle will not be as favorable as in recent decades. The evolution of rates in Japan, global asset inflation, the erosion of disposable income, tariffs in the US, etc. All this leads us to think that the cost of capital has changed; money is no longer free and that has enormous implications in many areas (valuations, private equity…). Europe is not badly positioned (low valuations, reforms, balance sheets are healthy) but we believe that investments require a more strict view on returns than ever.

Columbus in 2025: leading positions, Zegona and Siemens Energy. This year we have had two standout stocks in the fund. First, Zegona, the company that owns Vodafone Spain. The stock has risen 229% in 2025 and has also paid us an 11% dividend. It is now our largest position, almost 9% of the fund. The company has executed a very successful restructuring plan, cutting costs and selling its fiber assets, which has allowed it to improve its balance sheet and cancel 70% of its shares. We estimate it can generate around 500 million of FCF, nearly 12% of its value. We still see room for further operational improvement and consolidation opportunities that could increase its value. In parallel, we have also built a position in the German company 1&1, which could also benefit from telecoms consolidation. The other relevant stock has been Siemens Energy, up 132%. It is the global leader in power grid infrastructure and gas turbines, which are very necessary to cover incremental energy needs. The management team has done a good job increasing capacity and cleaning up Gamesa. In this case we doubled the position at the end of 2024 and have recently been trimming it at highs, but it still represents 6% of the fund.

Other interesting stocks: Fresenius, Prysmian, EFG, Unicaja and Mapfre. Fresenius (+46% in 2025) is a good example of a strong management team implementing an improvement plan on a quality asset, and it has good potential in a very high-growth area such as biosimilars. Prysmian (+37%) is the global leader in cabling for electrification, an area in expansion, with few competitors of similar scale. In financials we maintain a significant position in EFG International (+43%) and have partially reduced our stakes in Unicaja (+117%) and Mapfre (+73%), two institutions that have been improving earnings and profitability in recent years.

New ideas entering the portfolio: Laboratorios Rovi, Fagron, 1&1, Dia Supermercados…and more to be announced soon: over the year we have been building positions in several stocks where we see very high potential. Rovi is one of the best-managed companies in Spain; we know its management team very well, having helped with its IPO. We estimate that its operating cash flow could triple in 5 years, and that is not properly reflected in the market valuation. Fagron is the global leader in pharmaceutical compounding, an area with solid long-term drivers. It also grows by acquiring small companies that add value to its assets. Finally, Dia Supermercados has successfully restructured its stores; its proximity model is ideal for families and it has a good management team.

Mistakes and poor investments: inevitably, we make many mistakes and less successful investments. Perhaps one good thing this year has been exiting some problematic positions quickly, such as Mobico or YouGov. And this year we have suffered significantly in two positions we still hold: Edenred, the world leader in services such as meal vouchers, which has faced very harmful regulatory changes, although in this case we expect a recovery in the medium term. It remains a good business with barriers to entry. We have also suffered in Redcare Pharma, the European leader in online pharmacy; in this case we have increased the position because we believe it will deliver solid growth and margin improvement in 2026.

A market with enormous opportunities… good growth prospects: this year we have also spent a lot of time analyzing companies that, for various reasons, have had a tough year but are good businesses. In Europe there are companies that have fallen sharply in 2025 but are good businesses. We are monitoring them closely, and in some cases, we have started to buy, such as Laboratorios Rovi, where we believe profitability will improve significantly in the future. It is interesting to see that EPS growth prospects in Europe for 2026 and 2027 are relatively solid (e.g. Goldman forecast is +11%/+13% resp., adjusted for currency) while valuation remains reasonable (14.9x PE 2026).

We end our review of 2025 here. We believe we hold very good companies in the portfolio and have attractive opportunities for 2026 that we hope to take advantage of. Currently our portfolio on average offers a very reasonable valuation (15x PE 2026) with solid top line prospects (6% sales CAGR 2025-28, 9% EBITDA), very healthy operating margins (24%) and cash generation (7% FCF yield).

Please, see below our monthly report for December:

Performance – December 2025. In December 2025, the Pareturn Columbus Class I2 fund rose by 2.8%, close to the European Stoxx 600 index, which gained 2.7%. Overall, the fund in 2025 was up 25.2%, outperforming the Stoxx 600 and the MSCI Midcap Europe Index. Thanks to this solid performance, the fund ranks in the first quartile of its category over 1, 3 and 5 years, according to Morningstar and Citywire data. Since its launch in June 2008, the fund has gained 217%, consistently beating the main European equity indices.

Market environment. a good month after a solid year: December ended positively after a strong year in 2025, though for global investors the US$ devaluation has eroded a good part of the gains. In Europe, the Stoxx 50 index rose 1.8% in December and it enjoyed a favorable return in 2025 (19%). In global markets, the main feature was the solid performance across markets, although the US$ decline wiped out a good part of the gains in the year.

Macro key topics:. Two topics have dominated 2025, the issues around the US$ and questions on the US budget deficit and its cost of financing, and the debate around AI. These two topics are likely to persist and most likely will continue to drive capital flows into other markets with better risk/reward. Long‑term bonds, always an important reference, showed some relief at the end of the year, reducing some pressure on government balance sheets.

Performance of Key Positions: During December, the most notable positions included: Dia Supermercados (+21%), Unicaja (10%), Laboratorios Rovi (+7%) y Bodycote (10%), some are recent additions to the fund, we have recently made relevant changes. On the negative side, there were somewhat sharp declines in Craneware (-11%), and AutoTrader (-8%) where we have a residual position.

Portfolio Changes: During December, partial adjustments were made to holdings with strong share‑price appreciation, including the received dividend from Zegona (11% yield). We have been actively monitoring several new ideas, some if which have made it to the portfolio in 2025, such as Laboratorios Rovi, Dia Supermercados, 1&1 and recently Fagron, a world leader in pharmaceutical compounds, a company with a solid management team and strong tailwinds to drive solid and profitable growth.

Download monthly factsheet [PDF]

Since May 2023, Spanish investors can access the Columbus strategy through the Spanish fund GVC Columbus European Equities FI. The Fund can be purchased through the AllFunds, Inversis and Fundsettle platforms. Columbus has a Master-Feeder structure. The Pareturn GVC Gaesco Columbus European Equity Fund in Luxembourg (master) and the GVC Columbus European Equities FI (feeder). The Luxembourg vehicle offers institutional and retail share classes denominated in euros and sterling.